Reckoning tide rises

Any downgrade, or even a negative outlook revision, raises sovereign borrowing costs and makes infrastructure capital more expensive to service.

Text size

Any downgrade, or even a negative outlook revision, raises sovereign borrowing costs and makes infrastructure capital more expensive to service.

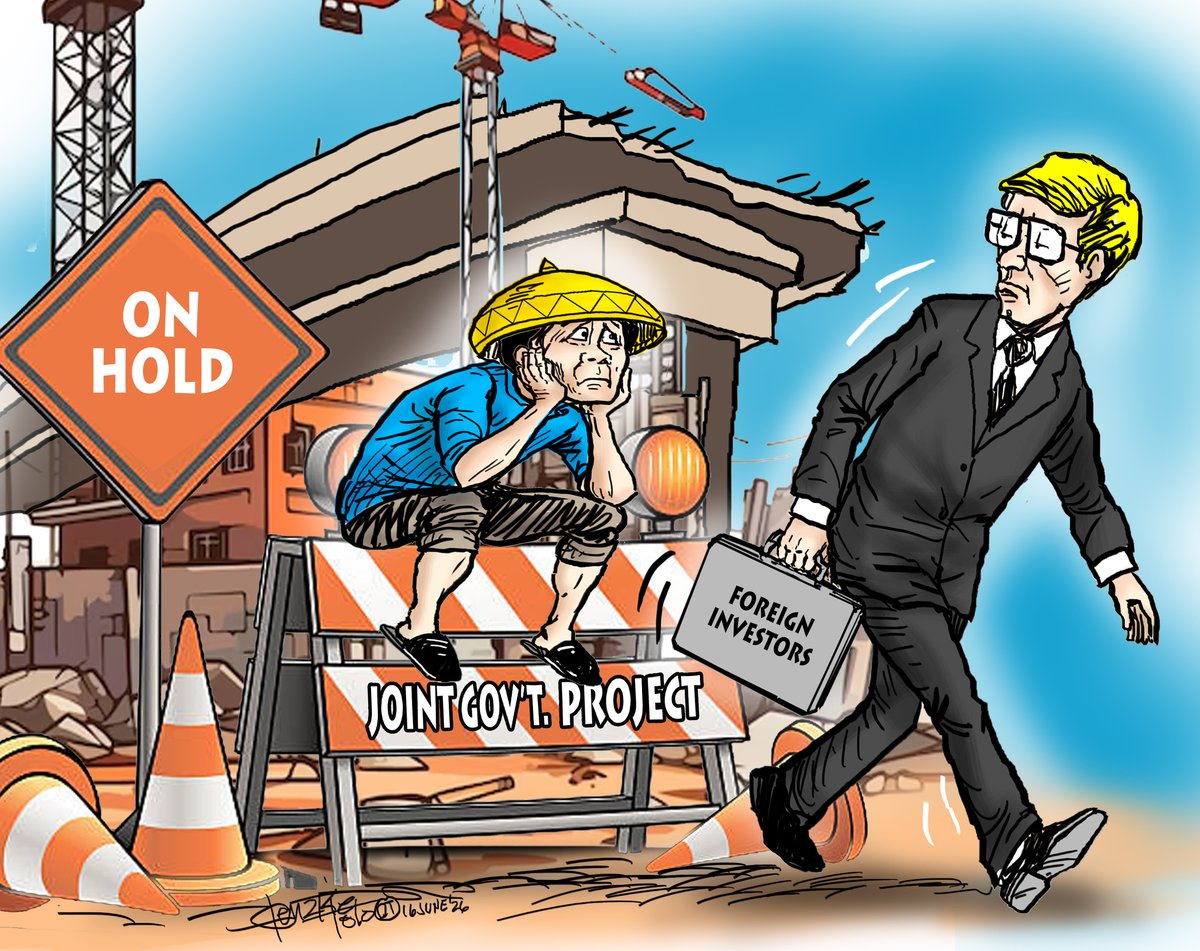

The Marcos administration might as well say farewell to investments in its Build Better More campaign after the damning assessment by the powerful Organization for Economic Cooperation and Development (OECD) of corruption in infrastructure projects.

The poor governance report has rippled across several fronts.

Credit rating agencies Moody’s, Fitch and S&P Global routinely incorporate governance risk into their assessments.

The report by the OECD, which comprises the world’s largest industrialized nations, cited a local study quantifying corruption losses of up to P118 billion annually in flood control alone.

The University of the Philippines Center for Integrative and Development Studies (UP-CIDS) estimated that kickbacks from rigged contracts may have caused losses ranging from P42 billion to P118 billion.

Any downgrade, or even a negative outlook revision, raises sovereign borrowing costs and makes infrastructure capital more expensive to service.

The fastest-growing class of infrastructure capital globally is Environmental, Social and Governance-mandated funds from pension capital, sovereign wealth and development finance institutions.

They are contractually prohibited from deploying into high corruption-risk environments.

The OECD report, coming from a body whose imprimatur big investors rely on, effectively flagged the Philippines as a jurisdiction requiring enhanced due diligence.

Many funds will simply move on to less complicated markets rather than absorb the compliance cost.

The Marcos administration’s growth strategy leans heavily on public-private partnerships (PPP) to plug the infrastructure financing gap.

Foreign concessionaries with the capital and technical capacity the government needs conduct rigorous political risk assessments before committing capital.

An OECD finding that PPP contracts lack embedded anti-corruption clauses and that local government units lack the capacity to implement environmental and social safeguards is precisely the kind of red flag that scuttles interest.

Its consequence is longer due diligence timelines, demands for stronger government guarantees, or outright withdrawal from bidding.

The Asian Development Bank, World Bank and Japan International Cooperation Agency from where the country draws infrastructure funds have their own standards that mirror OECD recommendations closely.

When the OECD documents that a significant share of flood control contracts went to a small number of firms and directly to crooked pockets and that some projects were non-existent or poorly executed, conditionalities are tightened, disbursements slow down, or will require independent third-party monitoring.

Vietnam, Indonesia and India are all competing for the same pool of infrastructure investment capital.

The OECD report covers Central and Southeast Asia, meaning investors can directly benchmark the Philippines against its neighbors.

Capital that might have flowed toward Philippine flood control, transport and energy infrastructure will predictably flow elsewhere.

The report makes explicit what should be obvious but is apparently not to the Marcos administration, which is that corruption in flood control spending wastes money and consequently destroys climate resilience in a country that ranks among the world’s most typhoon-exposed.

International climate finance mechanisms, from the Green Climate Fund to Just Energy Transition Partnerships, impose governance preconditions that the Philippines would be hard-pressed to meet.

It also risks being locked out of concessional financing precisely because it cannot guarantee that funds won’t be siphoned off before a single structure is built.

What the OECD report tells foreign investors is that procurement is opaque, audits are insufficient, contract data is unpublished and budget releases are untethered from verified completion in the Philippines.

Investment risk premium on the Philippines will remain elevated.

The flood control scandal has already cost the country up to P118 billion a year but the cost in foregone investments may ultimately be larger.